This week the downward effects of cold fronts up north brought some chilly weather to the islands. Most locals turned their heat on for the first time in many months. With daytime highs in the 60’s to low 70’s, an even chillier weekend is forecast. While northern states are slated for lots of snow, temperatures here both Saturday and Sunday are expected to go only into the mid-50’s, with freeze warnings in some of SW Florida. Certainly not bikini weather, though most vacationers make the best of it, while we locals continue to enjoy wearing our once-a-year clothes. On a positive note, there were a couple of evenings with nice sunsets again this week. All now after 6 p.m. Hooray!

At SanibelSusan Realty

After posting our blog last week, The SanibelSusan Team had a busy real estate weekend. Teammate Dave and I both fielded inquiries and offers. Wed, we received a new condo listing which already is generating interest with showings scheduled before guest check-in tomorrow. Thank goodness, our photographer, Jim Anderson, fit us into his busy schedule with him filming it this morning. Fingers crossed that he will Photoshop the sky which today looks like I remember it in New England when it was about to snow.

Tues, we had a nice closing this (the results of a multi-year group effort Lisa, Dave, Susan). Two more closings are in the works for next week. Phones are ringing with prospective buyers, many worried, as we are, about the limited inventory. We also are meeting with prospective Sellers next week hopefully to boost that inventory.

The details on activity since last Friday, in the island MLS, are after a couple of news items below.

Florida Realtors® Update – What’s Changing for Florida Real Estate?

Posted Jan 21 on Florida Realtors® by Marla Martin:

Posted Jan 21 on Florida Realtors® by Marla Martin:

“2022 RE Trends panel: Big and small biz relocations, plus the here-to-stay wave of untethered remote workers, will impact Fla.’s markets for years to come.

“ORLANDO, Fla. – After almost two pandemic years, changes created to deal with COVID-19 have created major shifts that affect Florida’s real estate markets, according to a panel of site developers, Realtors® and economic development experts who spoke to more than 300 Realtors during the 2022 Florida Real Estate Trends summit Thursday.

““Prior to COVID, we saw a lot of Wall Street firms testing the waters with CEOs looking at homes,” said Kelly Smallridge, president and CEO of the Business Development Board of Palm Beach County. “Now, these CEOs are signing seven- to 10-year commercial leases, they’re legally domiciling and, most importantly, they’re buying homes and putting their kids in private schools. We now have zero slots open for any private school in Palm Beach County.”

“The Real Estate Trends event was part of this year’s Florida Realtors®’ Mid-Winter Business Meetings at the Renaissance SeaWorld Orlando. In addition to Smallridge, other panelists included: Deanna Armel, broker-owner, Armel Real Estate; John Boyd, principal, The Boyd Company; and Melanie Schmees, director of business and economic research, Greater Naples Chamber of Commerce. Florida Realtors Chief Economist Dr. Brad O’Connor and Dr. Jessica Lautz, vice president of demographic and behavioral insights at the National Association of Realtors (NAR) also shared their insights on the 2022 outlook.

“Kelly Smallridge, president and CEO, Business Development Board of Palm Beach County – Unfortunately, the misconception that Florida schools lag and the state’s educated workforce is lacking still lingers among many executives inquiring about relocating their businesses, Smallridge said, and that is “absolutely not the case.” Once they’re in Florida, check out the schools and have their children tested for placement, their perception quickly changes, she said. “The average salary in Palm Beach County is $61,000, while the average salary of the people coming in now is $1 million,” she added – another boon to local businesses and area development.

Many of the business executives interested in moving to Florida want to look at homes first, she said, and may not mention a possible relocation. “When you’re taking a buyer around to see homes, see if they also have any interest in bringing a business here,” Smallridge advised brokers and real estate agents. “You can offer them information to connect with local chambers of commerce or economic development officials. We help them understand all the logistics of what it takes to get them up and running. So, we’re really part of your team. Together, we can land not only the home but the company as well.”

“Melanie Schmees, director of business and economic research, Greater Naples Chamber of Commerce – Like real estate, economic development often involves referrals and regional cooperation, said Schmees. “Naples is a unique market,” she explained. “Right now, we have a 1% industrial vacancy rate; sometimes, we need to direct those interested to other areas near us like Fort Myers. The whole region benefits.” One factor important for ongoing business relocations and continued economic development in Florida will be the consideration of employees’ needs and how they can manage new lives here. “We need to create an environment that works for the workers, not only the business executives,” Schmees said. “Often, their workers are concerned that they can’t make the move. They’re worried they can’t find housing or figure out their cost of living.”

“Deanna Armel, broker-owner Armel Real Estate – “Florida in general is a draw for business and for out-of-state buyers,” she said. “There’s no state income tax, our weather, beaches, and in Orlando, our theme parks. Since COVID (the start of the pandemic), home preferences have changed. People want an office, a pool, flex space and a yard.” According to Armel, the influx of major business relocations and wealthy buyers who can pay cash – like many California residents moving to Florida after selling their homes – has made an impact on the housing market, particularly in the luxury-home sector. “I call it monopoly money,” she said. “Cash is great, but it’s really hurting our buyers who need financing, our veterans, our workers and first-time homebuyers. The competition is unbelievable, especially in new construction. New construction, turn-key, luxury homes: That’s what California buyers want.”

“John Boyd, principal, The Boyd Company – Before the pandemic, about 10% of employees worked remotely, said Boyd. “Today, over half of the workforce works remotely, at least on a hybrid basis, and this change is here to stay. It saves businesses too much in terms of office space, operations and so on. It’s also a great recruiting tool – people like the flexibility.” He noted that economic development is now a “people first operation.” And that, he said, “has established a new class of economic development workers – the residential real estate agent.”

Brightline, the private high-speed rail system running from Miami to West Palm Beach with an expansion in the works to Orlando, is a positive for marketing Florida for economic development, the panelists said. “I think we’ll see a lot of exciting development projects along those Brightline lines, with the ability to connect between Central Florida and South Florida,” Boyd said. Another plus for Florida? “Our state is a magnet for global talent, experience and skill sets,” he added. “Having no state income also attracts industry and development. Business and money tend to go where it feels welcome.””

Loans for Condos? New Rules Start to Have an Effect

Posted on-line Jan 24 at Florida Realtors®, the below article is sourced to the “Daily Breeze” and mortgage broker Jeff Lazerson:

Posted on-line Jan 24 at Florida Realtors®, the below article is sourced to the “Daily Breeze” and mortgage broker Jeff Lazerson:

“Fannie’s tighter loan requirements post-Surfside collapse started Jan. 1; Freddie’s start Feb. 28. In the meantime, the list of no-loan condo projects will likely keep growing.

“HERMOSA BEACH, Calif. – A nightmare scenario looms for condo buyers applying for certain types of federally backed mortgages. If you are selling or are looking to buy an attached condominium in a community with five or more attached units, conventional financing from mortgage giants Fannie Mae and Freddie Mac may soon become elusive.

“HERMOSA BEACH, Calif. – A nightmare scenario looms for condo buyers applying for certain types of federally backed mortgages. If you are selling or are looking to buy an attached condominium in a community with five or more attached units, conventional financing from mortgage giants Fannie Mae and Freddie Mac may soon become elusive.

“Beginning Jan. 1 for Fannie and starting Feb. 28 for Freddie, the mortgage giants are putting the screws to a required HOA questionnaire. New questions ask applicants about the structural integrity of the community and whether any code violations are anticipated.

“No doubt, Fannie and Freddie’s updated lender mandates are in response to the Florida condo tower that killed 98 people last June 24. Years of deferred maintenance at the Champlain Towers in Surfside caused the 12-story building to collapse.

“No doubt, Fannie and Freddie’s updated lender mandates are in response to the Florida condo tower that killed 98 people last June 24. Years of deferred maintenance at the Champlain Towers in Surfside caused the 12-story building to collapse.

“Answering the agencies thoroughly and completely could force lenders to decline a mortgage application. (Remember: Mortgage lenders fund a loan, and then may sell it to Fannie or Freddie).

““Yes, lenders are declining projects even for a simple special assessment for repairs now. Things are just trickling in right now because the guidance started Jan. 1,” said one condo project approval expert, who asked to remain unnamed because he’s not the media spokesman for his company. “Soon enough we’ll see the effects hit all the condo market. I’ve only seen it affect projects with major issues at this point; meaning (the project) has code violations and millions of dollars of repairs underway.”

“Answering these questions honestly or possibly with a guess could bring liability in the form of future lawsuits against HOA stakeholders, such as the property management company, board members, inspectors, engineers and the association.

“If the questionnaire isn’t completely answered because the answers are unknown or undetermined, it might mean the purchase or refinance gets torpedoed.

“Here is a sprinkling of questions included in Fannie Mae’s Form 1076 condominium project questionnaire (posted December 2021 and updated to eight from five pages):

Question: Is the HOA aware of any deficiencies related to the safety, soundness, structural integrity or habitability of the project’s building(s)?

My take: If management didn’t know about any deficiencies, for example, and answered as such, should they have reasonably known these calamities could come up later?

Question: Is it anticipated the project will, in the future, have such violations (zoning ordinances, codes, etc., which are related to safety, soundness, structural integrity or habitability)?

My take: For the love of peace, how could one possibly determine if yet-to-be-written, jurisdictional codes trigger new violations in the condo complex?

“These dubious questions could be akin to a winning lottery ticket for any attorney who lives in the world of HOA litigation.

“Why is this so problematic? The nation has a huge community of really old condos and many of them are backed by Fannie Mae and Freddie Mac mortgages. The U.S. has as many as 156,000 condo associations and cooperatives housing between 27 million and 32 million Americans, according to the Community Associations Institute (CAI).

““Seventy percent of all condo loans in the U.S. are Fannie or Freddie (backed),” said Dawn Bauman, senior vice president of government affairs at CAI. “Sixty to 70% of all condo complexes are more than 30 years old.”

Fannie Mae has a published list of 82 “unavailable” California condo-projects, including the Marina City Club in Marina Del Rey, which has $80 million to $140 million in needed repairs according to a report last year. That a 10-acre complex is one of nearly 1,000 “unavailable” condo projects nationwide. To Fannie Mae, unavailable means a property is ineligible for purchase by the agency.

“One mortgage executive told me Fannie is making the rounds, emphasizing these new condo questions during lender visits. So don’t be surprised if that unavailable list explodes as Fannie collects more intel.

“To be fair, Fannie and Freddie need to dig more deeply to assess and consider condo structural risk before purchasing those mortgages from lenders. The mortgage giants also may disqualify a condo community for other reasons, such as a lack of budget reserves.

“If your loan is denied over the Fan or Fred HOA certification answers, you may be able to get funded on what the industry calls a non-warrantable loan. You should expect to pay perhaps one-half to one point higher in rate than conventional financing. You also might have to provide a larger down payment or have more remaining equity compared with Fannie-type requirements.

“But buyer beware: Non-qualified mortgage lenders that offer the exotic non-warrantable condo mortgages are not a loan approval shoo-in, either.

“For example, California-based LendSure has a condo guidance checklist to help determine investor risks. The common three items it looks at are investor concentration (how many rentals are in the complex), single investor (does one person or entity own a bunch of the units), and litigation against the condo complex, according to Joe Lydon, co-founder, and managing director of LendSure.

“Why so much deferred maintenance? Unit owners are often resistant to increased HOA fees or special assessments for repairs and updates.

“Condo complex building inspections can run $15,000 to $50,000 depending on the number of units, according to Bauman.

““Community Associations Institute is lobbying for laws mandating reserve studies and building inspections,” said Bauman. CAI is also asking Fan and Fred to give HOAs more time to be able to address so many of the new HOA questions. “Five years to ramp-up the requisite building inspections.””

Sanibel & Captiva Islands Multiple Listing Service Activity January 21-28, 2021

Sanibel

Sanibel

CONDOS

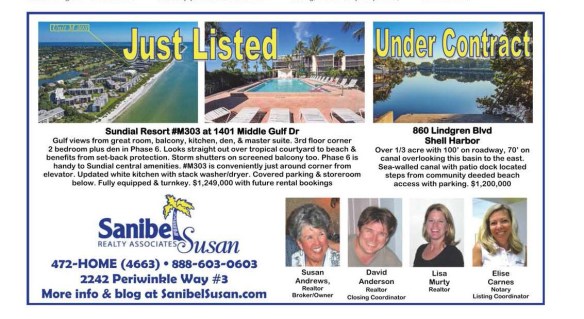

7 new listings: Loggerhead Cay #351 2/2 $824K; Lighthouse Point #112 3/2 $864K; Sanibel Moorings #1332 2/2 $874,999; Sanibel Moorings #122 2/2 $1.2M (our listing); Shell Island Beach Club #A5 2/2 $1.2M; Pointe Santo A2 2/2 $1.35M; Sedgemoor #101 3/3.5 $3.995M.

Boardwalk to beach at Sanibel Moorings

1 price change: Gulfside Place #210 2/2 now $1.549M.

6 new sales: Sundial #I402 1/1 listed at $659K, Mariner Pointe #421 2/2.5 listed at $739.9K, Sunset South #11C 2/2 listed at $1.095M, Sand Pointe #218 2/2 listed at $1.099M, Sundial #M303 2/2 listed at $1.249M (our listing), Pointe Santo #A2 2/2 listed at $1.35M.

To beach from Sundial East

2 closed sales: Nutmeg Village #308 2/2 $1.225M, Gulfside Place 124 2/2 $1.45M.

HOMES

4 new listings: 645 Oliva St 3/3 $1.1M, 593 Lake Murex Cir 3/3 $1.395M, 5802 Sanibel-Captiva Rd 3/3.5 $1.495M, 4717 Rue Belle Mer 3/3 $4.95M.

No price changes.

5 new sales: 2030 Sunrise Cir 3/3 listed at $1.625M, 489 Sawgrass Pl 5/5 listed at $2.15M, 1266 Par View Dr 4/4 listed at $2.295M, 435 Bella Vista Way E 3/3 listed at $5.2M, 3767 West Gulf Dr 4/4.5 listed at $7.5M.

3 closed sales: 6429 Pine Ave 3/2 $869K, 1943 Sanibel Bayous Rd 3/3 $1.125M, 2379 Wulfert Rd 4/4.5 $2.495M (our buyer).

LOTS

Nothing to report.

Captiva

CONDOS

No new listings, price changes, or new sales.

1 closed sale: Marina Villas #706 2/2 $950K.

HOMES

No new listings or price changes.

1 new sale: 14865 Mango Ct 2/2 listed at $1.295M.

No closed sales.

LOTS

Nothing to report.

This representation is based in part on data supplied by the Sanibel & Captiva Islands Association of Realtors® Multiple Listing Service. Neither the association nor its MLS guarantees or is in any way responsible for its accuracy. Data maintained by the association or its MLS may not reflect all real estate activity in the market. The information provided represents the general real estate activity in the community and does not imply that SanibelSusan Realty Associates is participating or participated in these transactions.

Below is our ad from today’s “Island Sun”.

Until next Friday. Stay warm! Susan Andrews, aka SanibelSusan

There was no Association of Realtors® Caravan Meeting this week, but early Tuesday the Professional Development Committee met. Guess who got up early to make 16 mini-strawberry shortcakes for us to enjoy after singing “Happy Birthday” to our Assoc Prez-Elect. He was grateful and his members appreciate that he volunteers his time, especially at 8:30 a.m. on his bday..

There was no Association of Realtors® Caravan Meeting this week, but early Tuesday the Professional Development Committee met. Guess who got up early to make 16 mini-strawberry shortcakes for us to enjoy after singing “Happy Birthday” to our Assoc Prez-Elect. He was grateful and his members appreciate that he volunteers his time, especially at 8:30 a.m. on his bday.. Next Thursday is the island Association of Realtors® July Monthly Breakfast Meeting. Speaker is Lee County Commission (former Sanibel Mayor) Kevin Ruane, who will update members on county initiatives and the causeway project. Following the meeting there will be a Realtor Caravan of new listings.

Next Thursday is the island Association of Realtors® July Monthly Breakfast Meeting. Speaker is Lee County Commission (former Sanibel Mayor) Kevin Ruane, who will update members on county initiatives and the causeway project. Following the meeting there will be a Realtor Caravan of new listings.

Bailey’s General Store Adds Vehicle Charging Station just east of the main entrance near the community bulletin board. It has two charging points to accommodate two vehicles at the same time and can charge all brands of electric vehicles. The store is open daily 7 a.m. to 7 p.m.

Bailey’s General Store Adds Vehicle Charging Station just east of the main entrance near the community bulletin board. It has two charging points to accommodate two vehicles at the same time and can charge all brands of electric vehicles. The store is open daily 7 a.m. to 7 p.m. Sanibel

Sanibel

I hope you had a safe happy July 4th holiday. Sanibel festivities were terrific with the morning weather perfect – bright sunny, with slight breeze, when the parade passed by the office.

I hope you had a safe happy July 4th holiday. Sanibel festivities were terrific with the morning weather perfect – bright sunny, with slight breeze, when the parade passed by the office.

I was busy meeting a contractor early yesterday so missed the Realtor® bi-weekly Caravan Meeting. Just one property was on tour for viewing after the meeting. The activity posted since last Friday in the Sanibel & Captiva Islands Multiple Listing Service follows some news below.

I was busy meeting a contractor early yesterday so missed the Realtor® bi-weekly Caravan Meeting. Just one property was on tour for viewing after the meeting. The activity posted since last Friday in the Sanibel & Captiva Islands Multiple Listing Service follows some news below. The chorus Holiday Concert will be Wednesday December 7 at 7 p.m. in BIG ARTS Christensen Auditorium.

The chorus Holiday Concert will be Wednesday December 7 at 7 p.m. in BIG ARTS Christensen Auditorium. Sanibel

Sanibel

Luckily, the heavy rains last weekend, didn’t cause much long-term flooding and it resulted in some terrific shelling for those enthusiasts. Now that the ground is saturated, islanders will be keeping a close eye on future rainy events. Meanwhile, the Anchor Dr bunnies are loving the juicy vegetation at my house. There were two munching in my yard this morning as I headed out to work. I love those little guys!

Luckily, the heavy rains last weekend, didn’t cause much long-term flooding and it resulted in some terrific shelling for those enthusiasts. Now that the ground is saturated, islanders will be keeping a close eye on future rainy events. Meanwhile, the Anchor Dr bunnies are loving the juicy vegetation at my house. There were two munching in my yard this morning as I headed out to work. I love those little guys! Some good news at the Sanibel & Captiva Islands Association of Realtors® Caravan meeting yesterday. As incoming Association Prez, Realtor® Greg Demaras mentioned in his opening remarks, there has been 100% increase in Sanibel home listings compared to ten days ago when there were only 11 homes for sale. (Actually, today the number of Sanibel homes available according to the islands MLS is up to 26. More inventory is becoming available.)

Some good news at the Sanibel & Captiva Islands Association of Realtors® Caravan meeting yesterday. As incoming Association Prez, Realtor® Greg Demaras mentioned in his opening remarks, there has been 100% increase in Sanibel home listings compared to ten days ago when there were only 11 homes for sale. (Actually, today the number of Sanibel homes available according to the islands MLS is up to 26. More inventory is becoming available.) 2022 SCIS Designation Classes

2022 SCIS Designation Classes  or the first time and three Realtors® working on their renewal.

or the first time and three Realtors® working on their renewal. Posted Tues, Jun 7, 2022 by SCCF (Sanibel-Captiva Conservation Foundation). All sea turtle research and monitoring is conducted by trained individuals operating under Marine Turtle Permit #047:

Posted Tues, Jun 7, 2022 by SCCF (Sanibel-Captiva Conservation Foundation). All sea turtle research and monitoring is conducted by trained individuals operating under Marine Turtle Permit #047:

Sanibel

Sanibel Until next Friday,

Until next Friday,

Turtles and tortoises are on the move depositing their eggs. Winter birds are migrating north, along with the people-birds aka snowbirds, while our year-‘round avian friends including snowy plovers, herons, and owls also are producing offspring.

Turtles and tortoises are on the move depositing their eggs. Winter birds are migrating north, along with the people-birds aka snowbirds, while our year-‘round avian friends including snowy plovers, herons, and owls also are producing offspring. Yesterday was the May monthly membership meeting at the Association of Realtors®. No longer offered via Zoom, it was great to see more in-person attendees including a couple of new affiliates. Due to an unexpected speaker cancellation, the two meeting sponsors, David Wright from Sanibel-Captiva Community Bank (SanCap Bank) and David Arter from Private Client Insurance Services (PCIS) provided quick updates on their businesses.

Yesterday was the May monthly membership meeting at the Association of Realtors®. No longer offered via Zoom, it was great to see more in-person attendees including a couple of new affiliates. Due to an unexpected speaker cancellation, the two meeting sponsors, David Wright from Sanibel-Captiva Community Bank (SanCap Bank) and David Arter from Private Client Insurance Services (PCIS) provided quick updates on their businesses. Insurance – David Arter, PCIS, provided highlights from the Special Florida Legislative Session about property insurance that wrapped up late Wednesday. Though not signed into law just yet, the measures passed by lawmakers this week may not immediately reduce premiums, but they do get at the heart of the problem and will have a long-term positive effect on stabilizing insurance in Florida. It took lawmakers three days to debate, discuss, and ultimately pass some significant property insurance reforms that will go a long way in helping to alleviate Florida’s ongoing property insurance crisis. Some of the topics included:

Insurance – David Arter, PCIS, provided highlights from the Special Florida Legislative Session about property insurance that wrapped up late Wednesday. Though not signed into law just yet, the measures passed by lawmakers this week may not immediately reduce premiums, but they do get at the heart of the problem and will have a long-term positive effect on stabilizing insurance in Florida. It took lawmakers three days to debate, discuss, and ultimately pass some significant property insurance reforms that will go a long way in helping to alleviate Florida’s ongoing property insurance crisis. Some of the topics included: The same special session for insurance reform discussed above was expanded to include condominium reform in response to the tragedy in Surfside, FL last June. Lawmakers acted quickly on this, unanimously passing a Building Safety bill in both chambers. It provides several measures designed to increase building safety and prevent the types of issues that lead to the Surfside collapse. Specifically, the bill:

The same special session for insurance reform discussed above was expanded to include condominium reform in response to the tragedy in Surfside, FL last June. Lawmakers acted quickly on this, unanimously passing a Building Safety bill in both chambers. It provides several measures designed to increase building safety and prevent the types of issues that lead to the Surfside collapse. Specifically, the bill:

Wishing you a safe thoughtful Memorial Day weekend.

Wishing you a safe thoughtful Memorial Day weekend. Though the islands continue to need rain (heard on the local news that SW FL is about 5” behind normal accumulation), traffic now is nearly perfect with very few waits anywhere. Midweek, I did a quick drive-around to some of the island resorts and beach accesses. Plenty of parking everywhere and several hotels/condos had few cars.

Though the islands continue to need rain (heard on the local news that SW FL is about 5” behind normal accumulation), traffic now is nearly perfect with very few waits anywhere. Midweek, I did a quick drive-around to some of the island resorts and beach accesses. Plenty of parking everywhere and several hotels/condos had few cars. Island Seafood Market Sanibel recently opened at 2330 Palm Ridge Rd. Hours are Monday through Saturday 9 a.m. to 4 p.m. (closed Sundays). They advertise that they are family owned and operated, specializing in local seafood. They own their boats and catch their fish!

Island Seafood Market Sanibel recently opened at 2330 Palm Ridge Rd. Hours are Monday through Saturday 9 a.m. to 4 p.m. (closed Sundays). They advertise that they are family owned and operated, specializing in local seafood. They own their boats and catch their fish! Following up on last week’s post by SCCF that the 2022 sea turtle nesting season has begun (April through October), the first loggerhead turtle nest was spotted and staked Wednesday morning (April 27), the same day that the first nest was discovered last year. Don’t forget to keep the beaches clean and unlit after dark. More tips at

Following up on last week’s post by SCCF that the 2022 sea turtle nesting season has begun (April through October), the first loggerhead turtle nest was spotted and staked Wednesday morning (April 27), the same day that the first nest was discovered last year. Don’t forget to keep the beaches clean and unlit after dark. More tips at  At the J.N. “Ding” Darling National Wildlife Refuge, admission fees for Wildlife Drive remain the same after season ends. The $10 vehicle fee, however, is good for three days starting May 1 and running through September. Show receipt at entrance booth when returning. Daily fees for bikers and walkers remain $1 each visit for visitors age 16+.

At the J.N. “Ding” Darling National Wildlife Refuge, admission fees for Wildlife Drive remain the same after season ends. The $10 vehicle fee, however, is good for three days starting May 1 and running through September. Show receipt at entrance booth when returning. Daily fees for bikers and walkers remain $1 each visit for visitors age 16+. April Association of Realtors® Breakfast Meeting – Yesterday was the monthly breakfast meeting of the Sanibel & Captiva Islands Association of Realtors®. Speaker was J.P. Fraites, Florida Realtors® Public Policy Rep. He provided highlights from the 2022 Florida legislative session which ended last month and produced the largest state budget ever (well over $100 billion). He highlighted several items including great strides in affordable housing (particularly for first responders, teachers, and medical workers) and, of particular interest to islanders, a record $1.6 billion for various water quality initiatives.

April Association of Realtors® Breakfast Meeting – Yesterday was the monthly breakfast meeting of the Sanibel & Captiva Islands Association of Realtors®. Speaker was J.P. Fraites, Florida Realtors® Public Policy Rep. He provided highlights from the 2022 Florida legislative session which ended last month and produced the largest state budget ever (well over $100 billion). He highlighted several items including great strides in affordable housing (particularly for first responders, teachers, and medical workers) and, of particular interest to islanders, a record $1.6 billion for various water quality initiatives. Once the rainy season begins, the clear aqua-looking water disappears, but it’s still looking pretty now. Happy Friday!

Once the rainy season begins, the clear aqua-looking water disappears, but it’s still looking pretty now. Happy Friday! With limited rain since Florida’s storm season ended last fall, forecasters have reported fire danger for much of central and south Florida. Rainy season usually doesn’t begin until May, but with unusual weather events in many places in recent years, who knows what 2022 will bring.

With limited rain since Florida’s storm season ended last fall, forecasters have reported fire danger for much of central and south Florida. Rainy season usually doesn’t begin until May, but with unusual weather events in many places in recent years, who knows what 2022 will bring. There were a couple of Association of Realtors® sponsored events this week with a Flood Insurance Seminar at the Community House Tuesday evening. With presentations from two Sanibel & Captiva Islands Association affiliate members, Dave Arter with Private Client Insurances Service and Chris Heidrick with Hedrick & Co. Insurance, the focus was the National Flood Insurance Program (NFIP) new FEMA (Federal Emergency Management Agency) 2.0 Rating System for flood insurance. It recently went into effect to more fairly charge flood rates. Unfortunately, on barrier islands like Sanibel and

There were a couple of Association of Realtors® sponsored events this week with a Flood Insurance Seminar at the Community House Tuesday evening. With presentations from two Sanibel & Captiva Islands Association affiliate members, Dave Arter with Private Client Insurances Service and Chris Heidrick with Hedrick & Co. Insurance, the focus was the National Flood Insurance Program (NFIP) new FEMA (Federal Emergency Management Agency) 2.0 Rating System for flood insurance. It recently went into effect to more fairly charge flood rates. Unfortunately, on barrier islands like Sanibel and  Captiva, that usually means higher premiums. Presenter examples often included a former $800 annual premium jumping to $8,000. Luckily, the new system limits increase to 18% per year.

Captiva, that usually means higher premiums. Presenter examples often included a former $800 annual premium jumping to $8,000. Luckily, the new system limits increase to 18% per year.

Posted online Tuesday, March 28, 2022 on FloridaRealtors® and sourced to Realtor.com, 2022 INFORMATION, INC. Bethesda, MD.

Posted online Tuesday, March 28, 2022 on FloridaRealtors® and sourced to Realtor.com, 2022 INFORMATION, INC. Bethesda, MD. Until next Friday,

Until next Friday,

It was good news to read the below article in today’s “Island Sun”. This approval has been long in coming.

It was good news to read the below article in today’s “Island Sun”. This approval has been long in coming. “The seawall at Spanish Cay borders the manmade canal separating it from Beachview Estates. Repairs to the seawall bordering a narrow walkway required commission approval of a long form development permit.

“The seawall at Spanish Cay borders the manmade canal separating it from Beachview Estates. Repairs to the seawall bordering a narrow walkway required commission approval of a long form development permit.

So, as we continue to market for new listings, today the magic inventory number is 12. According to the Sanibel & Captiva Islands Multiple Listing service, now there are just 12 condos and 12 homes for sale on Sanibel, while on Captiva, there are 12 in total (4 condos plus 8 homes).

So, as we continue to market for new listings, today the magic inventory number is 12. According to the Sanibel & Captiva Islands Multiple Listing service, now there are just 12 condos and 12 homes for sale on Sanibel, while on Captiva, there are 12 in total (4 condos plus 8 homes). Next week, I will be attending a “Florida Real Estate Trends” update by Florida Realtors® Chief Economist Dr. Brad O’Connor. He is scheduled to update policymakers, residents, and Realtors® on what is ahead in 2022. Real estate drives Florida’s economy and as the COVID-19 pandemic continues into its second year, it sure would be nice to know what lies ahead.

Next week, I will be attending a “Florida Real Estate Trends” update by Florida Realtors® Chief Economist Dr. Brad O’Connor. He is scheduled to update policymakers, residents, and Realtors® on what is ahead in 2022. Real estate drives Florida’s economy and as the COVID-19 pandemic continues into its second year, it sure would be nice to know what lies ahead.

Happy New Year! Wishing your good health & safety, happiness & colorful sunsets in 2022!

Happy New Year! Wishing your good health & safety, happiness & colorful sunsets in 2022!